What Does Charged-Off Mean With Regard to Debt?

What Is Charged-Off Debt?

Missing payments or paying your creditors late may not seem like a big deal, but the reality is that it can have significant financial and credit consequences. If you miss payments too many times, your creditor may charge-off the debt. When your debt is charged-off as bad debt, not only will it impact your credit, but it does not end your financial obligation to pay the debt.

If you're wondering what it means to have a debt charged-off, we've gathered information to help you understand the process, what it means for your credit, and how to address a charged-off debt.

What Happens During a Credit Report Charge-Off?

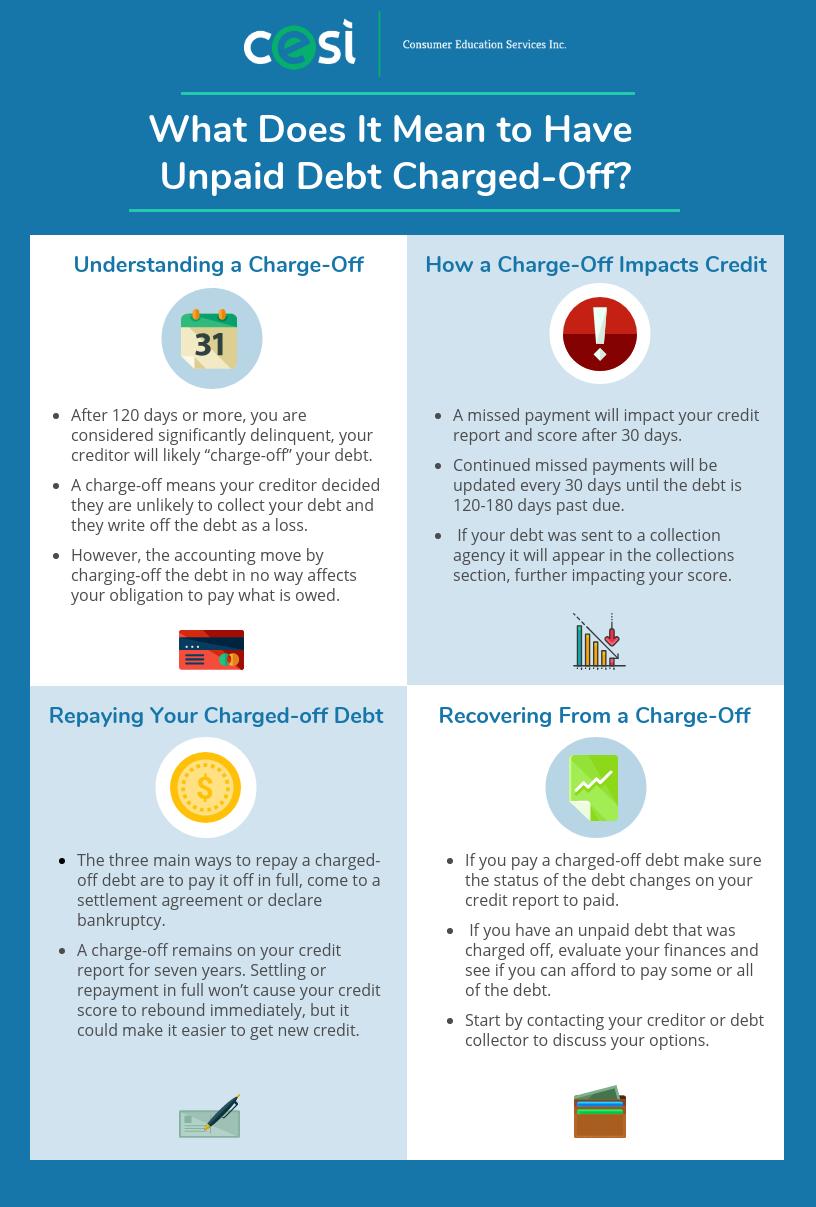

A debt charge-off occurs when you don’t make at least the minimum payment to your creditor for too long. Typically, if you've gone more than 120-180 days without making payments on your debt, the creditor will charge it off. This means that the creditor will stop their internal collection attempts and assume that you will not be paying the debt according to your credit agreement.

In a debt charge-off, the creditor removes the debt from their books and lists it as a loss for their accounting purposes.

Once your debt has been charged-off, the creditor will close your account, and in most cases, they will either sell or transfer your debt to a collection agency.

Understanding Charged-Off Debt Infographic

Download a copy of our infographic

How Does Charged-Off Debt Impact My Credit?

Having a debt charged-off will impact your credit in significant ways. In order for your debt to be charged-off, your payments will have been delinquent for a lengthy amount of time. Each time your payment is 30 days late to your creditor, it will be reported to the credit bureaus. One single late or missed payment impacts your credit score. If you consider the impact of 6 months or more of missed payments, your credit score will have dropped significantly by the time you reach charged-off status.

In addition to late payments, a charge-off is listed on your credit report. One reported charge-off can substantially impact your credit score.

A credit score that has been lowed by missed payments and charged-off debt can carry long-term consequences including, but not limited to:

- Increased interest rates on existing and future credit

- Higher rates for insurance and utilities

- The need to pay larger deposits for items like rent and utilities

- Inability to obtain new credit

- Failure to qualify for home loans

- Impact to future employment

How Long Will a Charged-Off Debt Stay On My Credit Report?

Any negative information reported to your credit such as late payments or a charged-off debt, will stay on your credit report for seven years. The date will beging from the date of the last scheduled payment you failed to make.

Unfortunately, paying the amount of your debt that has been charged-off amount will not remove it from your credit report, although your credit report will be changed to “charged-off paid” or “charged-off settled."

At the end of 7 years, the charged-off debt will automatically fall off your credit report.

Am I Still Responsible for Charged-Off Debt?

If your creditor has written off your balance as "bad debt," that doesn't mean no longer have an obligation to repay that debt.

Once your account is charged-off by your creditor, it is typically transferred to a collection agency. The collection agency may represent the original lender, or the agency may purchase your debt from your creditor. In this case, the collection agency will now become your creditor. The collection agency will then attempt to recover the debt, sometimes adding additional interest and fees. Because a debt collector has purchased your debt from the original creditor, the only way they recoup that investment is to collect from you, which unfortunately often means that a debt collector will be more aggressive in their collection attempts.

Whoever ends up with your charged-off debt, you are still responsible for repayment of the debt according to the terms of your lending agreement. That agreement will remain until you have paid the debt in full, or until you have reached a settlement agreement (allowing your to pay less than the full balance) with the owner of your debt.

Debt that has been sold can get confusing, so it's important to understand who owns your debt before you make payments.

How Can I Avoid Debt Charge-Offs?

Because of the impact to your credit, you will want to avoid having any of your credit accounts charged-off. Debt can quickly spiral out of control, and the more you get behind with payments, if can be difficult to catch up. Check out our helpful infographic resource: 8 Signs You Need Help Managing Debt for more information.

It's important to maintain healthy financial habits that will lead to financial success. If you are having a hard time making at least your minimum monthly payments, contact your creditors right away and communicate with them instead of avoiding the issue. In some cases, your creditors may make payment arrangements with you. This can help you get back on track and avoid a debt charge-off.

In the event of a serious financial hardship, your creditors may have internal hardship programs to help you avoid a significant delinquency in your payments.

If you are experiencing financial difficulty and are looking for a solution, non-profit credit counseling can help you make sense of all your options. Credit counseling agencies are here to help with debt—whether it’s helping you create a workable monthly budget or explaining your various debt relief options.

Our counseling is confidential and there’s never any obligation. Contact us today for a free financial assessment with one of our certified credit counselors

OUR MISSION

Consumer Education Services, Inc. empowers people to overcome their financial challenges and lead financially-healthy lives.

Our Services

Registered 501(c)(3). EIN: 56-2106758